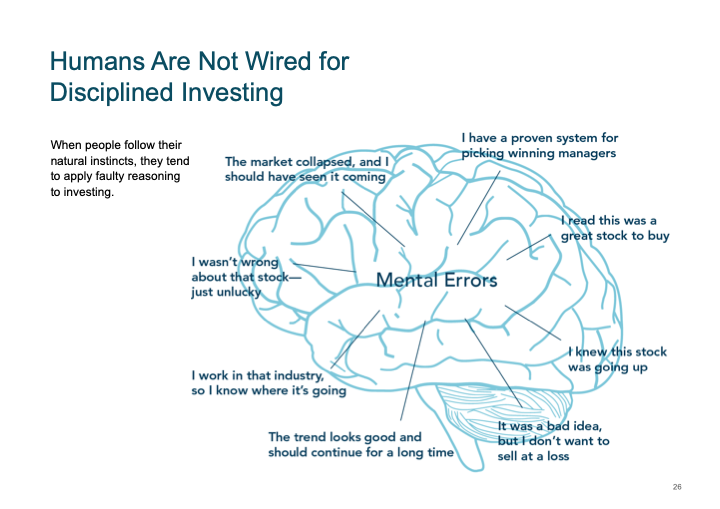

You And Your Worst Enemy

According to Benjamin Graham, one of the greatest investors of all times you are likely to be your own worst enemy and not the “jackals” of the financial industry.

“The investor’s chief problem - and even his worst enemy - is likely to be himself.”

Why could he think like that?

Well, because investors…

The 7 stages of Financial Enlightenment

The following is by Alex Riley, Bunker Riley Financial Planning, UK and I felt it so relevant to our reality that I quote the full content with his permission.

“We live in a world of instant gratification. Waiting more than 2 minutes for anything these days is an injustice. And here I am asking for five.

Google, Amazon, YouTube and Netflix exemplify the demands of ‘I want it now’ consumerism. It permeates everything, including financial advisory goals. Swathes of savers and investors want immediate results but rarely want to put in the work to understand how achievable that is. Ambitions are often misguided, and reality won’t dawn for those investors until they experience the 7 stages of financial enlightenment.

“Swathes of savers and investors want immediate results but rarely want to put in the work to understand how achievable that is.”

Whichever way you cut it, financial success is a long-term journey requiring introspection and life-long adjustment. Maybe you’ll catch a lucky break, but the reality is that there are no shortcuts. So here is a guide to financial enlightenment, as I see it, broken down to 7 stages.

1. Self-Management

People starting out on their financial journey self-manage. It’s natural to take care of basics as they arise such as joining a company pension. But others make a conscious decision to DIY invest through personal accounts managed online. Without the expertise to recognise what constitutes a good outcome, or after having experienced an expensive mistake, self-management often leads to confusion.

2. Confusion

If it’s not clear how you’re getting on because you have nothing to compare against, or if it’s obvious that you’ve made some mistakes, you’ll eventually conclude that confusion reigns. You’ll ask questions of yourself. If I’m an educated, intelligent person following the financial news, then why isn’t this working? What did I miss? Am I even doing this right? Why am I underperforming? Why are my friends doing so well? What’s their strategy? This is harder than I thought. I’m not getting the results I deserve. Confusion often leads to being overloaded.

3. Overloaded

The feeling of stress and helplessness weighs heavy. You’re trying to stay on top of your finances but there’s always something else to do. Your finances have progressed beyond your current capabilities. You haven’t got the time or inclination to do it properly now. You’re overloaded because either your financial circumstances, emotional temperament or lack of time have taken their toll. The stakes might also be much higher now and you worry about making the same mistakes you did before. You know that offloading some, or all, of your burden will ease the strain, so this might be the time to start taking advice.

4. Taking Advice

You need help but paying for it feels painful. Questions abound over adviser integrity and value for money. All I’d say here is that a professionalfinancial planner works withyou to ensure yourbest interests. They do not represent the financial ‘industry’ or work for the benefit of product providers. Choose wisely and a good, professional adviser will watch out for you. Collaborating with one will provide you with value at a multiple of their fee over time.

“Choose wisely and a good, professional adviser will watch out for you. Collaborating with one will provide you with value at a multiple of their fee over time.”

So, eventually, you decide to ante-up and pay for professional advice with the expectation that it will immediately absolve you of your financial woes. Wrong. You’ll certainly begin to get on track but you’re only halfway there. You’ve made a good decision but what you also need is an education.

5. Education

You’ll begin to understand that investing without a goal is like building a house without a blueprint. Your adviser will help you plan for and meet financial goals, backing up their advice with evidence and insight. You’ll get to understand how financial planning and investment markets reallywork. And there’s a big difference between that and the narrative asset managers push through sponsored media.

Your adviser will discuss with you, goals, contribution rates, taxes, why costs matter, what is and isn’t controllable, how behaviour significantly affects outcomes, the randomness of investment markets, risk, how pundits, expert and media opinion are for the most part useless and how the best definition of wealth is really planning for ‘funded contentment’ and not about ‘getting rich’. Only after many years of seeing the real world in action through this newly educated financial perspective will you come to a new realisation.

6. Realisation

With new knowledge comes the realisation that the more we know, the less we understand. There are too many moving parts to be able to have complete certainty and there is not a perfect financial plan or investment solution.

“The more we know, the less we understand.”

So, do you give up? Of course not. Better to plan for all eventualities than not at all. You keep planning, learning and investing but stop relying on unrealistic forecasts or those who express complete certainty. In doing so you become free from the shackles of general financial commentary which portrays finance as clear-cut, with no grey. You no longer pay attention to what other people think. You have reached the point of enlightenment.

7. Enlightenment

Congratulations! You now know what is important to you. You understand that your financial plan is different from everyone else, so you’ve stopped comparing. You know what you can and cannot control as well as what offers the highest probability of success. You can spot hyperbole a mile away. You’re humble about your own ability, understand the risk of poor outcomes and don’t take future returns for granted. You don’t stress over small details (should I invest 9% in Emerging Markets or 10?) instead spending time on the big problems which are likely to have a real impact. You take setbacks in your stride and can manage your expectations. You know that there is not a perfect solution, so you don’t waste any time or mental effort looking for one. ‘Good enough’ to reach your goals will do.

And understanding that good enough, and not perfect, will likely see you do better than 95% of other people out there is key. You don’t need to force a winner with the risk of going out of the game. Just keep the ball in play. But seeing is believing and it is not until you’ve experienced all 7 of these stages that you will reach the point of your own financial enlightenment.

Having read this fine and relevant content an important question emerges: You Hungarian and or regional reader what stage are you at?

Do you understand that you have a chance to reach the last stage than 99, 999 % of your fellow citizens.

But until then here are a couple of good advice for you:.

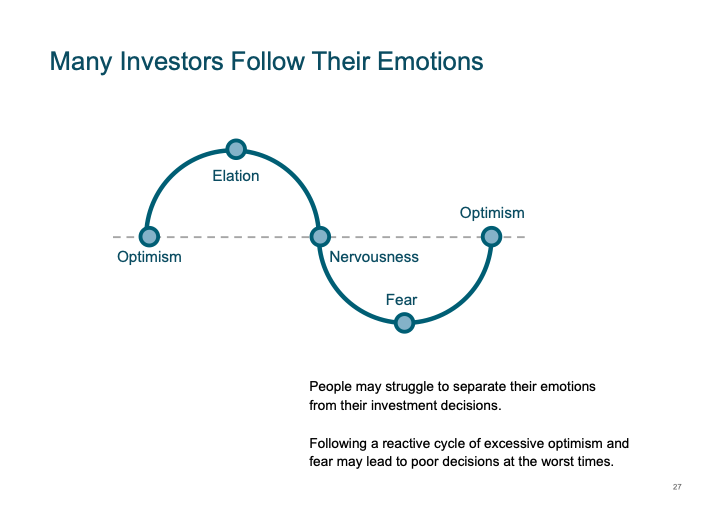

Manage Your Emotions!

Most people permanently struggle to remove emotions from their investment decisions, with little success. Markets fluctuate, sometimes up, sometimes down. Reacting to actual market events may result in bad investment decisions.Most people invest according to the emotional roller-coaster below whereas they should act without emotions no matter what.Just look at the horizontal dull face emoji under the roller coaster.

By Metis Ireland. Original concept by Andrew Nelligan.

Look Beyond The Headlines!

Daily financial media and commentaries may test your investment discipline provided you have such at all.Some piece of news are pessimistic about the future while others try to inspire you to act according to the latest investment fad. If the headlines confuse you, think it over where they come from, what they are based on and stick to your long term strategy.

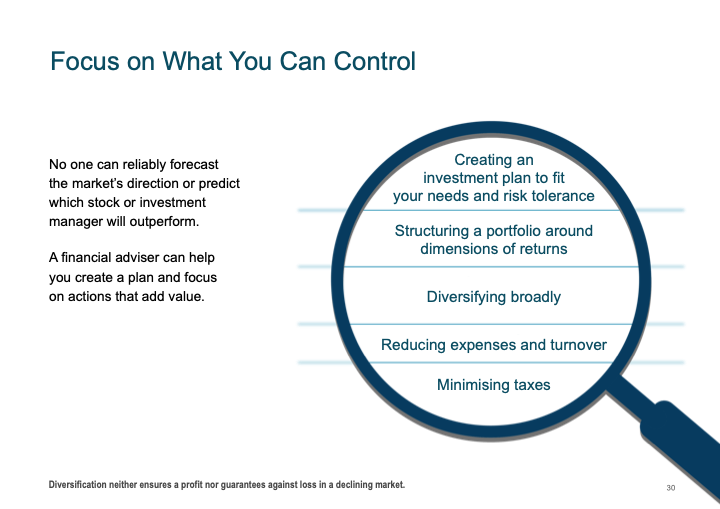

Focus on what you can control.

A real financial planner can assist you to focus on the following actions which mean added value for you and therefore lead to a better, more successful investment experience:

Prepare an investment plan to fit your needs and risk tolerance

Structure your portfolio around dimensions of risk

Diversify globally

Manage expenses, turnover and taxes

Stay disciplined